What the floor was really telling us

Humanoid Guide sent Leo Terry to Chicago for three days on the Automate 2026 floor, and he came back with more than a highlight reel. Between the keynotes, the market sessions and the demos, a clear picture formed of where automation actually is — and how far the humanoids still have to travel. This is his longer read behind the floor dispatch: the numbers, the framework he kept coming back to, and an honest look at the gap between a great demo and useful work.

The quarter behind the show

The market data presented on stage framed everything else. On paper Q1 looked flat, but that headline hid a sharp rotation: a steep drop in automotive masked broad-based growth almost everywhere else. Material handling — moving, picking, packing, palletizing — is now where the orders are.

Robot orders, machine-vision and cobot figures from the A3 market sessions; humanoid production from the Interact Analysis briefing. Q1 2026, North America unless noted.

Automation is moving in three phases

Walking the hall, the field sorted itself into three overlapping waves. Most of what is shipping today sits firmly in the first; the third is only just beginning to show up in buying patterns.

Specialised industrial robots

Deterministic machines built for one job — welding in hard-to-reach spots, palletising, painting, sanding. The early wins were all designed to plug straight into the existing workflow of the role they take over, mimicking the function rather than the human form.

Collaborative robots

Machines flexible enough to work alongside people in the same industrial space, replacing hard-labour roles. These need an AI layer built on top of the deterministic base to handle variation safely — and cobot orders are climbing fast.

Fully flexible humanoids

General-purpose platforms that can, in principle, do almost anything. The hardware is production-ready and the demos are impressive — but the brains still need far more data before they leave the demo stage for real shifts.

Four variables shape every product

Every machine on the floor — from a driverless forklift to a full-size humanoid — can be read against the same four levers. They explain why so much of what ships looks nothing like a human, and why the humanoids that do are still the hardest to deploy.

- Functionality. The early successes are ruthlessly specialised. A suction pad on a single arm moves boxes faster than two coordinated hands ever could — so most shipping robots optimise for the job, not the silhouette.

- Form. Today’s industrial machines bolt into the world as it already exists: a forklift without a driver, a 6–7-axis arm on a table. The open question is whether replacing the full lifecycle eventually produces designs that look radically different.

- Implementation. Right now robots conform to the factory. A growing chorus of investors and builders argues the factory should instead be redesigned around the robots — moving from fragile assembly lines to interconnected webs that limit downtime when something fails.

- Adaptivity. Machines can do almost anything, but adding a new skill still means costly retraining and manual tuning. The race now is to layer in-house AI models on top of safety protocols for faster, cheaper, more flexible adaptation.

Great hardware, unfinished brains

The most honest takeaway from the pavilion: the bodies are ready, the minds are not. Several of the most spectacular humanoid demos were, on close inspection, being driven by a person standing just off-stage with a remote. The vision-language-action and world models that would make them truly autonomous still need a great deal more data to mature.

How do you close the gap? The leading answer on the floor was data, gathered every way possible: robot “gyms” where a machine is hand-operated in a space that mimics its future job, blended with simulation, video, and anything else relevant — all inside a non-bypassable safety “tunnel” that lets the robot move freely without breaking past hard safety and capability limits.

Three ways to build a humanoid

Companies chasing the humanoid opportunity are placing their bets differently. The split is worth watching, because perfecting all four variables at once is what separates a demo from a deployable product.

Hardware-first

Pouring effort into best-in-class bodies. The platforms are remarkable — but the demos still lean heavily on teleoperation.

Software-first

Skipping the perfect chassis to build autonomous software on ready-made or off-the-shelf hardware instead.

Narrow-scope autonomy

A human form with limited but reliable actions, aimed squarely at structured, sterile industrial spaces.

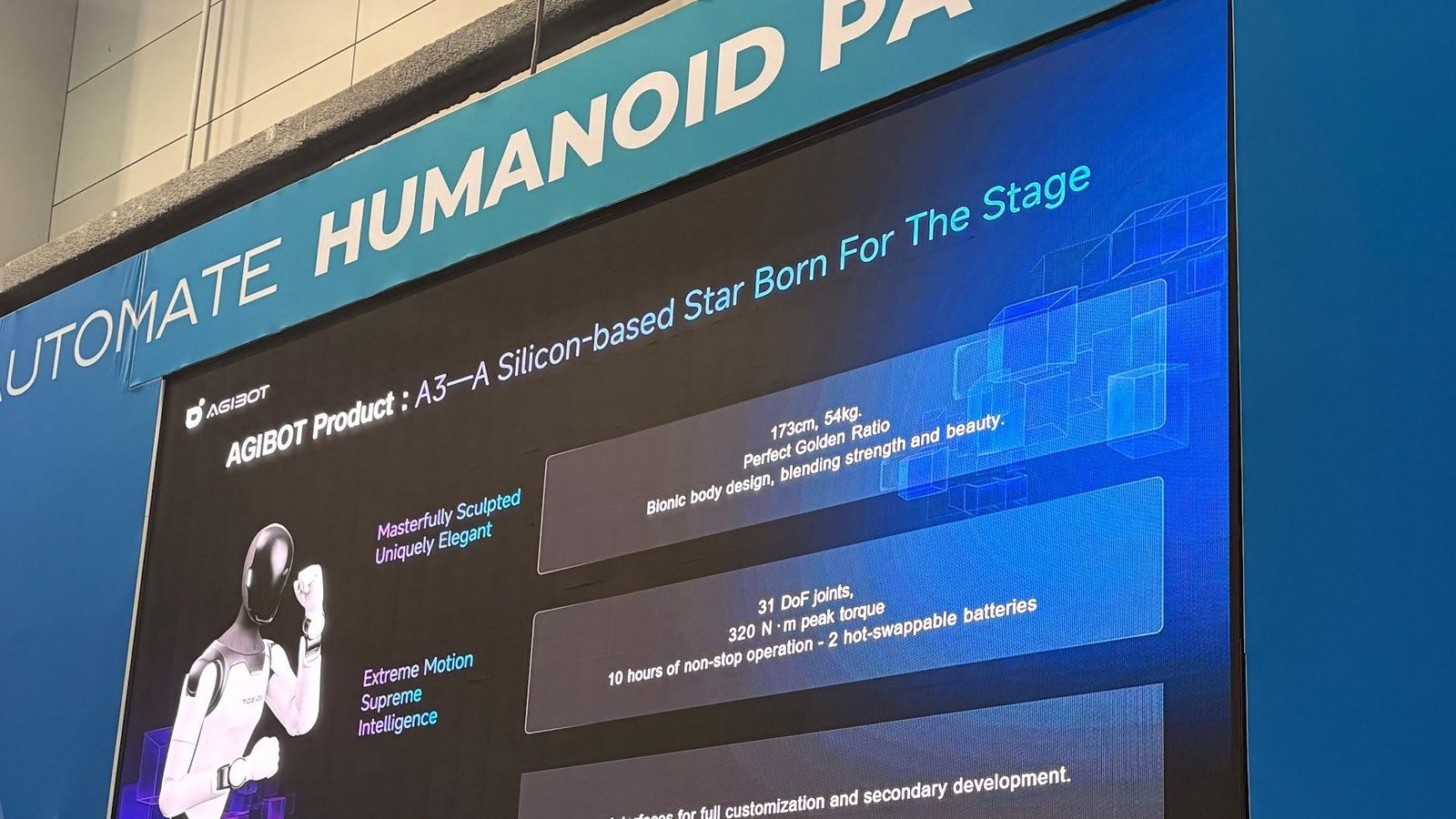

The most promising humanoid we saw on functionality, flexibility, design and speed-to-adoption was Neura Robotics. Versatile hardware spanning strength and delicate touch sensitivity, multiple form factors beyond the classic humanoid, and a well-judged brain that balances deterministic limits with a flexible AI layer on top. Their robot-gym training is time-intensive per client today — but reusing those workflows across new clients should compound as they scale toward a more general model.

Voices from the floor

Short, candid conversations with exhibitors between demos — straight from the show floor.

The constraints nobody could ignore

For all the optimism — the strongest sentiment readings in two years — the sessions kept returning to the things standing between today’s demand and tomorrow’s deployment.

The grid is the limiting factor

More than 2,060 GW of capacity is waiting to connect — about 1.6× the entire current US installed base — with a median wait approaching five years. Data centres alone are set to climb from 4.4% of US power in 2023 toward 12% by 2028.

Almost all magnets come from China

Roughly 91% of rare-earth processing and 85% of high-performance magnets originate in China — and 2025 showed how quickly that can be used as a trade lever. The US response is real, but early and defence-focused.

Capex is becoming a monthly bill

Robotics-as-a-service is moving from pitch to practice — the first public humanoid contract is paid per robot-hour, and AI is increasingly billed by the token. The largest buyers, meanwhile, are pulling integration in-house.

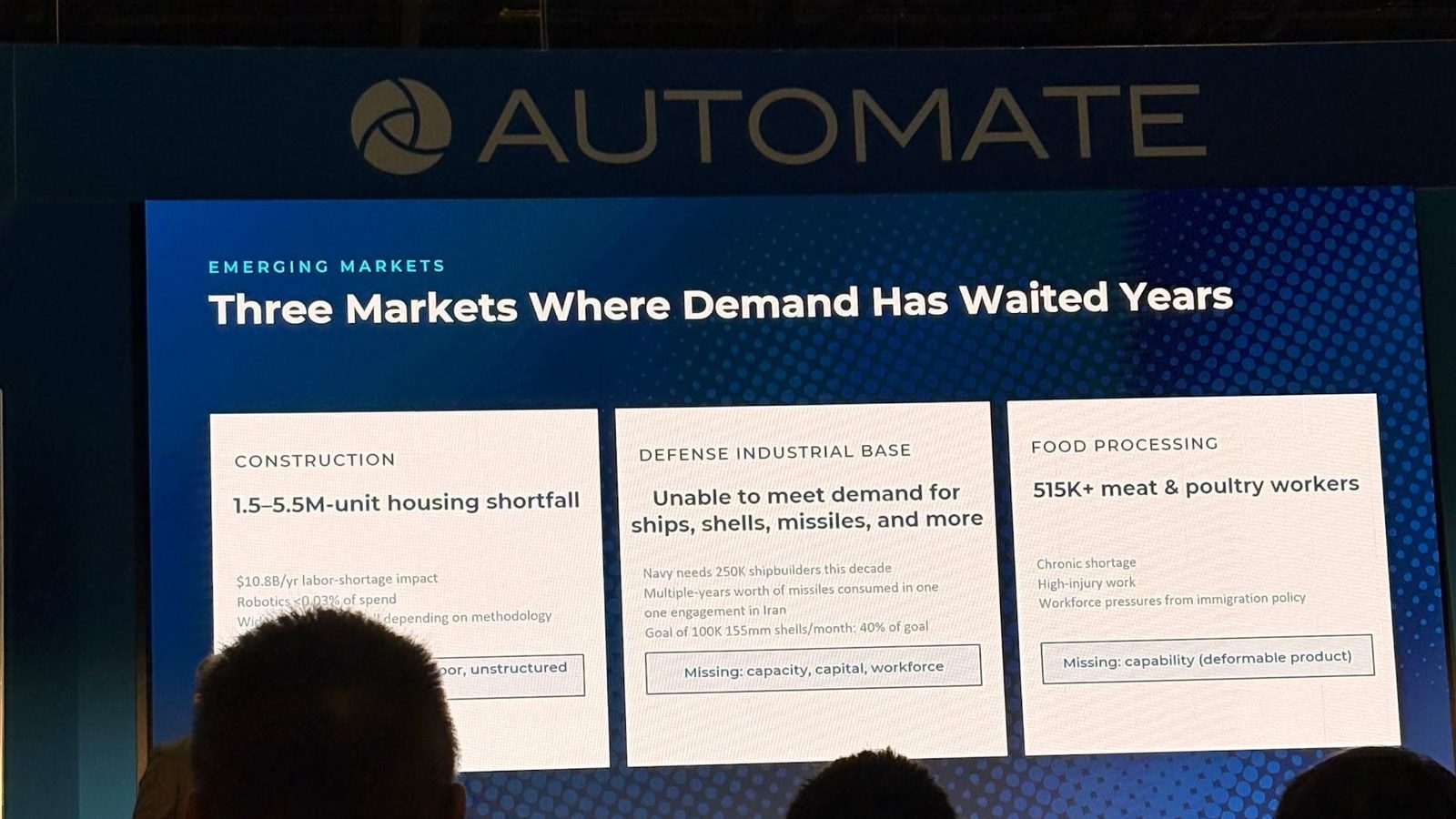

Three markets that have waited years

Construction faces a 1.5–5.5M-unit housing shortfall; the defence industrial base can’t meet demand for ships, shells and missiles; food processing is short 515k+ workers in high-injury roles. Each is waiting on capacity, capital or capability.

The full picture behind the floor

Funding, supply chain, leading manufacturers and forecasts — mapped in depth in our 2026 report.

Read the 2026 Market Report