The Humanoid Robot Supply Chain

The strategic window closes in 2027–2028.

The humanoid robot supply chain is consolidating. By 2027–2028, supplier positions across actuators, sensors, power, compute, and integration will lock in around dominant designs. This 226-page report maps the $38B opportunity and the playbook for Tier 1 and Tier 2 suppliers to claim their position before the window closes.

Why suppliers – and why now

The humanoid robot industry has reached an inflection point. The electromechanical competencies the automotive industry has developed over decades – precision actuators, sensor fusion, 48V power electronics, battery management, thermal systems, functional safety – are the precise capabilities humanoid robotics lacks at scale. This report maps that opportunity across fourteen dimensions and tells you, concretely, what to do about it.

Tier 1 system integrators

How to translate ASIL, ISO 26262, and IATF 16949 process maturity into a humanoid platform advantage Chinese competitors cannot replicate.

Tier 2 component suppliers

Where 48V architecture convergence creates direct adaptation pathways – and which entry points have 12–18 month time-to-revenue.

Actuator & motion specialists

Competitive landscape for harmonic drives, planetary roller screws, and frameless torque motors, and where the $9.86B actuator market is heading.

Sensor & perception suppliers

The largest uncaptured opportunity in humanoid robotics – and the playbook for unified perception platforms built on ADAS heritage.

Power electronics & battery makers

Why 48V mild-hybrid IP maps almost one-to-one to humanoid power systems, and the path from $14M to $851M by 2034.

Investors & corporate strategy

Where component pull will surge, which suppliers are positioned, and how to read the $3.7B in 2025 humanoid funding.

The central finding

Automotive suppliers hold decisive advantages in precisely the areas where humanoid robotics faces its most critical bottlenecks – reliability, functional safety, 48V power electronics, and sensor fusion. The strategic window for establishing supply chain position is narrow and closing. Chinese suppliers, already commanding 63–70% of the global humanoid supply chain with 30–40% cost advantages, are consolidating rapidly. The question is not whether humanoid robotics will create a substantial supplier market – it is which automotive suppliers will capture value before supply chain architectures fully consolidate in 2027–2028.

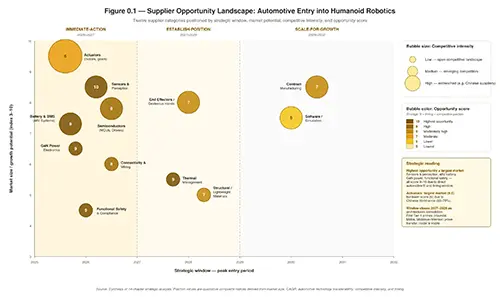

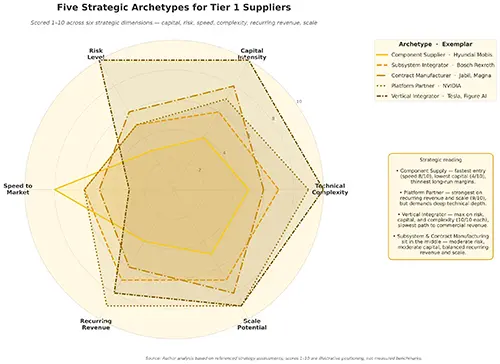

Five positioning archetypes

Not every supplier should enter the same way. The report defines five strategic archetypes, each scored across six strategic dimensions – capital intensity, time to revenue, competitive moat, technical risk, market size, and strategic optionality.

1. Component supplier

Adapt existing automotive components. Fastest time to revenue (12–18 months), lowest capital intensity.

2. Subsystem integrator

Deliver integrated actuator or sensor modules. Higher margin, leverages automotive systems engineering.

3. Technology licensor

License precision motion, BMS, or safety IP to humanoid OEMs. Asset-light path with patent protection.

4. Joint venture partner

Co-develop platforms with humanoid OEMs. Hyundai Mobis–Boston Dynamics demonstrates commercial viability.

5. Full Tier 1 humanoid

Become a Tier 1 system integrator for humanoids. Highest capital, highest reward, longest horizon.

What’s inside – 16 chapters

A complete strategic and technical reference. From actuators to AI compute, from regulatory frameworks to the U.S.–China contest, every chapter ties technology to business strategy and to the actions automotive suppliers should take in 2025–2027.

Executive Summary

The strategic imperative, supplier opportunity landscape, and consolidated market metrics across the entire humanoid value chain.

The Humanoid Robot Revolution

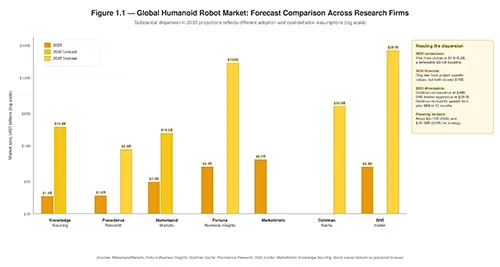

Market forecasts from seven research firms, adoption timeline by segment, regional distribution, and the structural drivers of demand.

Humanoid Robot Technology Architecture

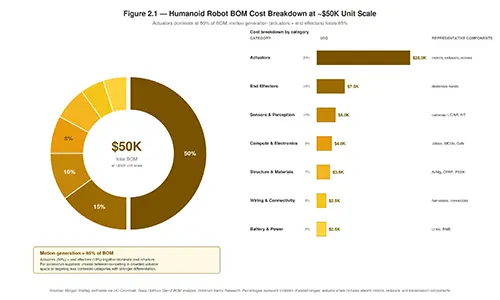

System architecture comparison across leading platforms, BOM cost breakdown at $50K unit scale, and where the dollars actually go.

Actuators and Precision Motion

The single largest BOM category. Competitive landscape for harmonic drives, planetary roller screws, and frameless torque motors.

Sensors and Perception

Force/torque, vision, depth, IMU, tactile. Why the sensor stack is the largest open platform opportunity in humanoid robotics today.

Battery Systems and Power Electronics

48V architecture convergence, cell chemistry choices, hot-swap and fast-charge requirements, and the BMS roadmap from EV to humanoid.

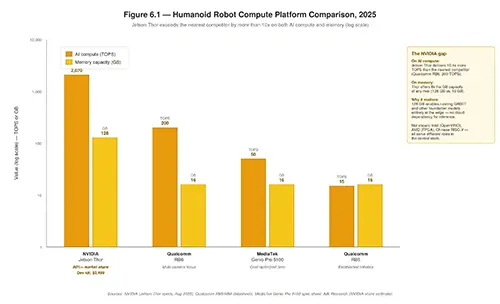

Semiconductors and AI Compute Platforms

Jetson Thor’s 2,070 TOPS, NVIDIA’s >80% compute share, GaN/SiC power, and the MCU race led by Infineon, Renesas, NXP, STM, and Microchip.

Structural Components, Materials, and Precision Manufacturing

Precision bearings, die-cast structures, sub-micron grinding, and the materials science behind a reliable humanoid skeleton.

Connectivity, Wiring Harnesses, and Communication Systems

EtherCAT, TSN, and the connectivity stack growing at twice the rate of automotive – and where harness fatigue limits robot reliability.

Thermal Management

From optional to mandatory above 500W. The $623M cooling market, micro-channel cold plates, and where Denso, Mahle, and Gentherm can play.

End Effectors

Robot hands – the hardest mechatronic challenge in the stack. Why this $2.88B market still has no dominant supplier.

Software, AI, and Simulation

NVIDIA GR00T, Figure Helix, Google Gemini Robotics, Skild AI, and the simulation stack reshaping how humanoids learn.

Tier 1 System Integration

The five strategic archetypes scored across six dimensions. Hyundai Mobis as the first proof point of the Tier 1 actuator model.

Regional Competitive Dynamics

The $46K vs. $131K BOM cost question, supply chain configurations, and how geopolitics reshape the cost landscape.

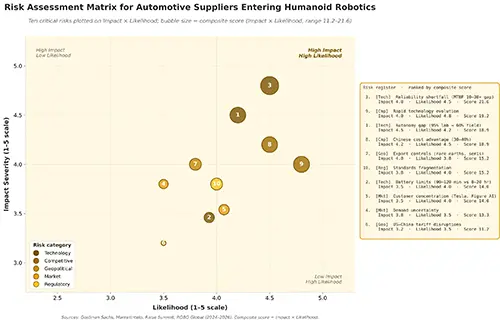

Regulatory and Compliance Framework

China’s national standard, the EU’s five-instrument stack, U.S. sector-specific oversight, and the risk assessment matrix every supplier needs.

Strategic Roadmap and Actionable Recommendations

The phased 2025–2035 roadmap with objectives, milestones, and KPIs for each phase – and supplier-category-specific action items.

27 figures. 49 strategic tables.

The report combines deep narrative analysis with the visual frameworks strategy teams need to communicate findings internally. Selected highlights:

Get the report

Single user license for individual analysts and consultants. Enterprise license for strategy teams, M&A groups, and supplier organizations.

Single User License

For one named analyst or consultant.

- Full 226-page report (PDF)

- All 16 chapters, 27 figures, 49 tables

- Single-user license

- Free updates throughout the 2026 cycle

- Email support for clarifications

Enterprise License

For strategy teams, M&A groups, and supplier organizations.

- Everything in Single User

- Unlimited internal users at one organization

- Right to quote in internal strategy documents

- Priority email support

- Briefing call with the author (optional, 60 min)

By purchasing, you agree to the terms of the license you select. Questions? human@humanoid.guide

Frequently asked questions

What you can expect from the report and how it differs from generic market research.

Who is the report written for?

Automotive Tier 1 and Tier 2 suppliers, component manufacturers, and the corporate strategy, M&A, and product teams inside them. It is also valuable to investors evaluating supplier exposure to humanoid robotics, and to humanoid OEMs sourcing components.

How is this different from the Humanoid Robot Market Report 2026?

The Humanoid Robot Market Report covers the full humanoid landscape – manufacturers, applications, consumer and enterprise demand, geopolitics. This report (The Humanoid Robot Supply Chain) is a focused supplier playbook: it goes deep on the supply chain, BOM economics, competitive landscape by component category, regulatory compliance, and what specific suppliers should do in the next 12–36 months to position themselves.

What is the methodology?

The report synthesizes data from Goldman Sachs, Morgan Stanley, McKinsey, Bain & Company, Counterpoint Research, MarketsandMarkets, ABI Research, Intel Market Research, and primary industry sources. Forecasts span 2025–2035. Every claim is cited; the appendix includes a full source index.

Will the report be updated?

Yes. Buyers of the May 2026 edition receive free updates throughout the 2026 cycle. Major revisions are released when material changes occur in the regulatory or competitive landscape.

Can I get a sample or preview?

Yes – the executive summary and chapter 0 are available as a free preview. Contact us for a sample PDF or briefing.

Do you offer custom research or briefings?

Yes. We provide tailored research and live briefings for supplier strategy teams. Get in touch to discuss scope.

The strategic window closes in 2027–2028

Chinese suppliers are consolidating position now. This is the playbook for automotive suppliers who intend to be part of the humanoid supply chain when it locks in.

Buy full report $590 · Just ReleasedNew! 2026 Humanoid

Robot Market Report

198 pages of exclusive insight from global robotics experts — uncover funding trends, technology challenges, leading manufacturers, supply chain shifts, and surveys and forecasts on future humanoid applications.

now Google DeepMind